Executive Overview

The 2026 State of Agriculture Resilience survey shows clear progress in regenerative agriculture programs, alongside persistent constraints. From our survey of more than 20 organizations across the global food and ag sector, four signals stand out that will define the year ahead:

Together, these findings point to an industry that understands the need to build resilience but is still figuring out how to execute at scale. The companies making the most progress are those aligning climate risk assessment with investment decisions, building fit-for-purpose data systems, and designing partnerships that reduce complexity rather than add to it.

This report dives deeper into these three levers, exploring where the industry stands today and highlighting the tactics most likely to drive progress in 2026.

From ESG to enterprise risk management

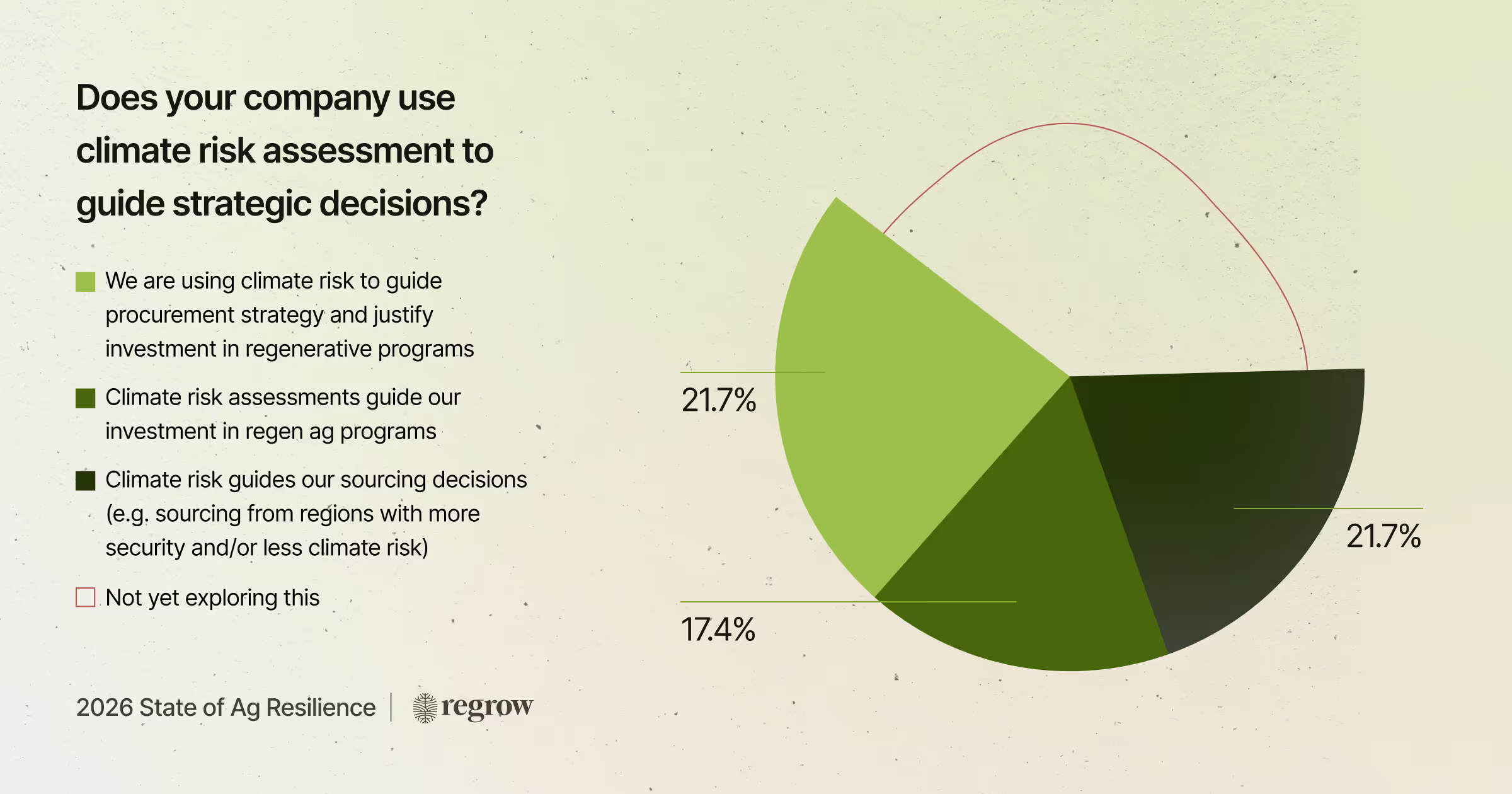

Climate risk assessments are increasingly shaping how companies prioritize regenerative agriculture investments and make sourcing and procurement decisions. Once treated primarily as disclosure exercises, risk assessments are now being used by leading organizations as active decision-making tools.

Survey results show that 60% of leaders are using climate risk assessments to guide program investment, sourcing decisions, and procurement strategy.

These companies are deploying regenerative agriculture as a practical lever for managing exposure in high-risk crops and regions, stabilizing long-term supply, and supporting farmers amid growing volatility. By translating climate hazards into business-relevant impacts, risk assessments help connect regenerative action to return on investment.

At the same time, nearly 40% of respondents have not yet integrated climate risk into strategic decision-making, often due to data limitations, internal alignment challenges, or uncertainty about where to start. For these organizations, climate risk is identified but underutilized, representing unrealized potential to strengthen resilience.

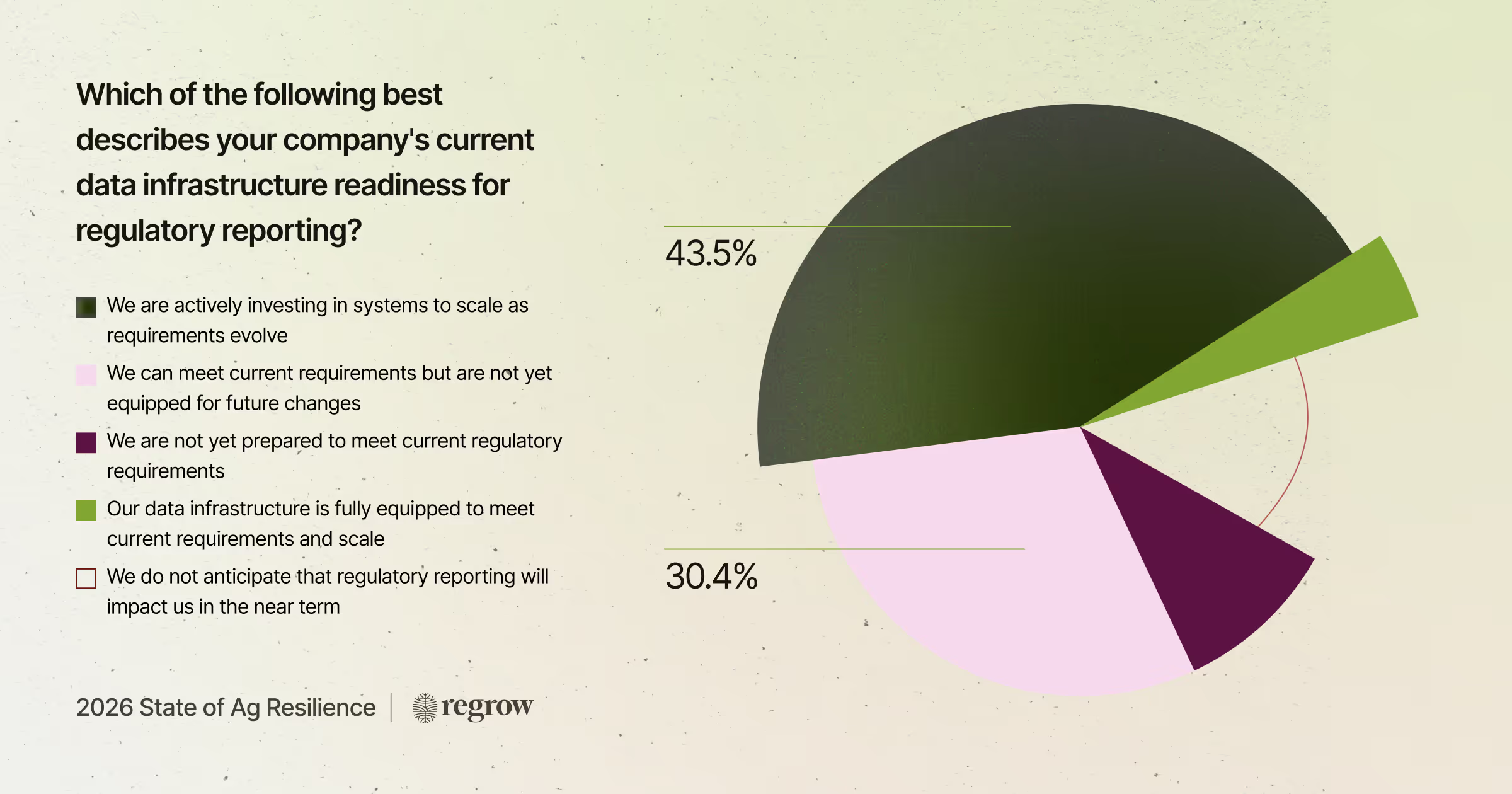

Data is no longer the question. Execution is.

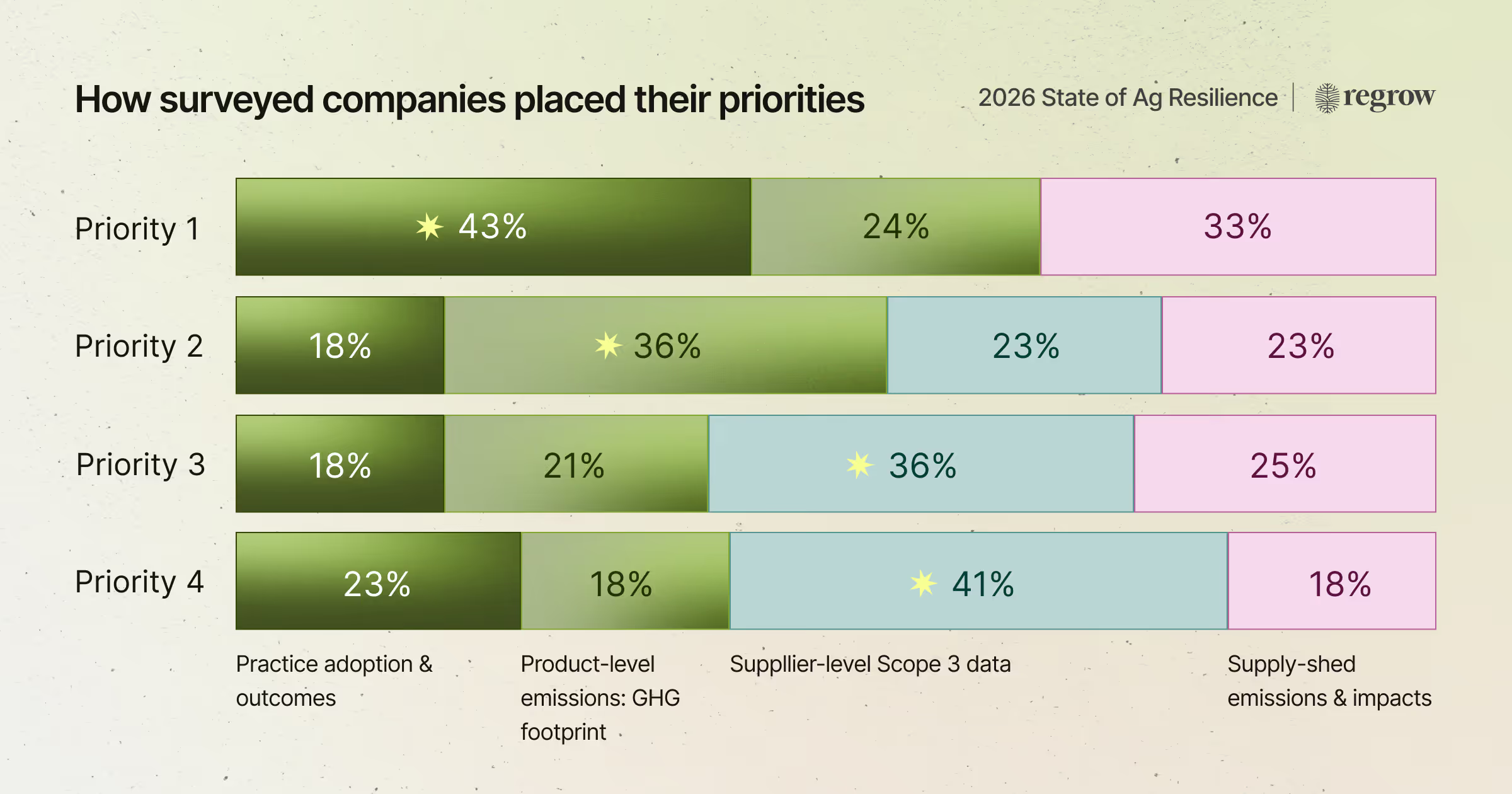

Companies show strong alignment on the data that matters most: practice adoption and outcomes, supply-shed-level emissions and climate data, and product-level greenhouse gas footprints. Yet access to this data across fragmented supply chains remains a central constraint.

When it comes to preparedness for reporting, one respondent reported being fully prepared to meet current regulatory requirements while also having systems in place to scale for future needs. Most organizations describe themselves as able to meet today’s expectations, but uncertain about how their data systems will adapt as guidance evolves. Despite this uncertainty, nearly half of respondents are actively investing in data infrastructure, signaling a critical transition moment.

Leading companies are beginning to adopt fit-for-purpose data strategies, aligning different levels of data rigor with different decisions. Rather than pursuing maximum precision everywhere, they are matching data quality to program maturity, reporting needs, and business use cases, allowing them to scale programs more efficiently while maintaining credibility.

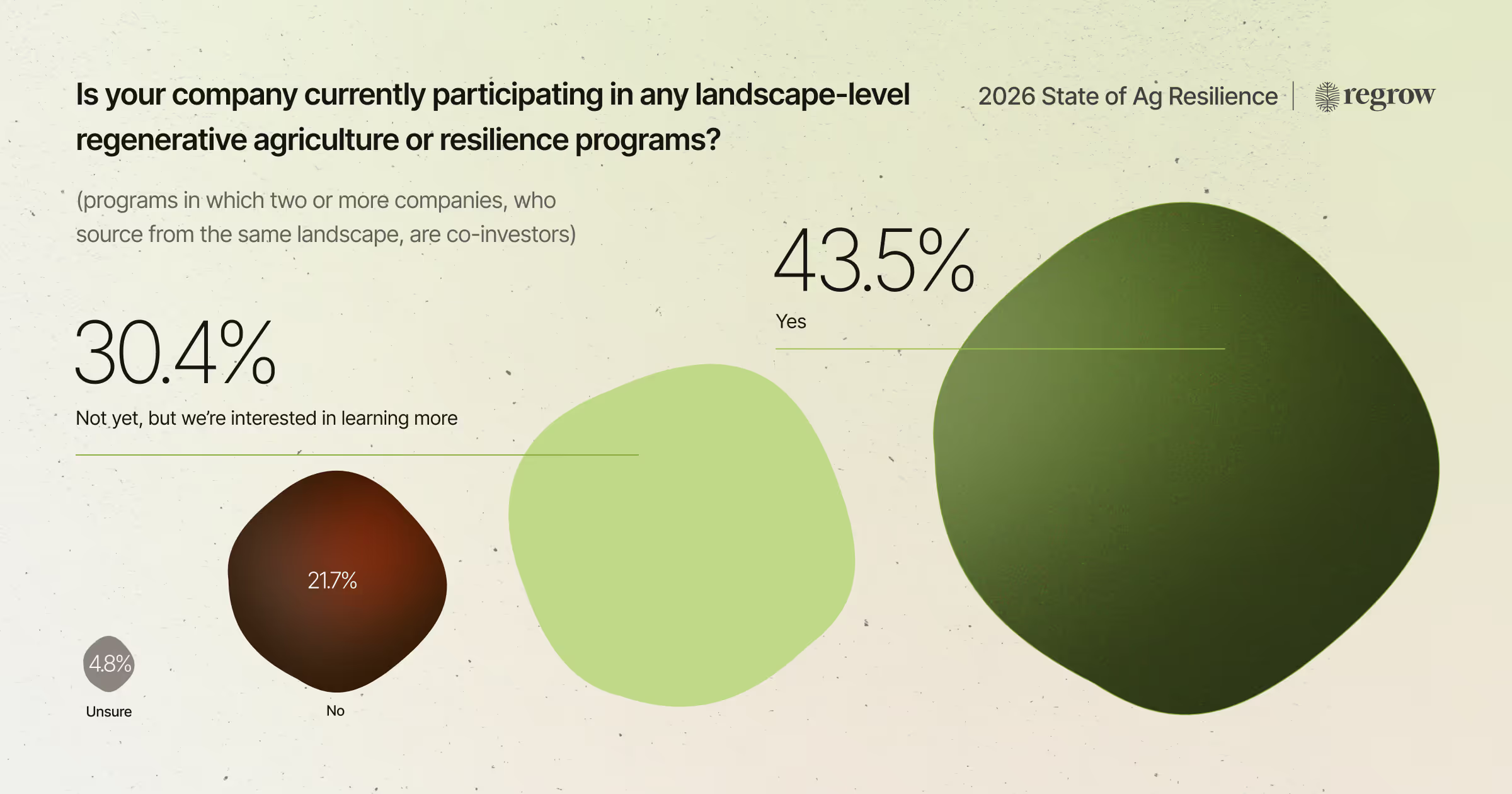

The case for landscape action is settled. The operating model isn’t.

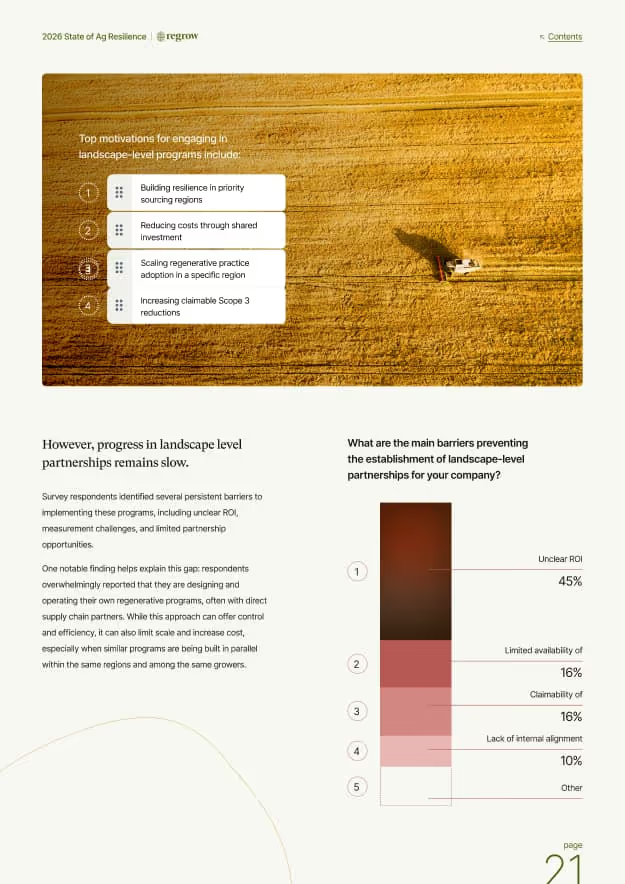

Interest in landscape-level partnerships is clearly growing as companies recognize that climate risk, soil degradation, and reporting complexity cannot be addressed through single-buyer programs alone. Survey respondents consistently pointed to shared investment models as a way to reduce costs, scale adoption of regenerative practices, and build resilience in priority sourcing regions.

However, execution remains uneven. Most respondents continue to operate their own regenerative programs, often in parallel with others in the same regions. While this approach offers control, it limits scale and increases cost. The primary constraints are internal: unclear ROI, measurement challenges, and misalignment across procurement, finance, and sustainability teams.

Successful partnerships share common traits: clarity on which collaboration model fits the sourcing context, early alignment on goals and metrics, and clearly defined roles across funding, farmer engagement, data collection, MRV, and reporting. The next phase of progress will depend less on proving the value of collaboration and more on designing partnership models that align incentives and make participation easier.

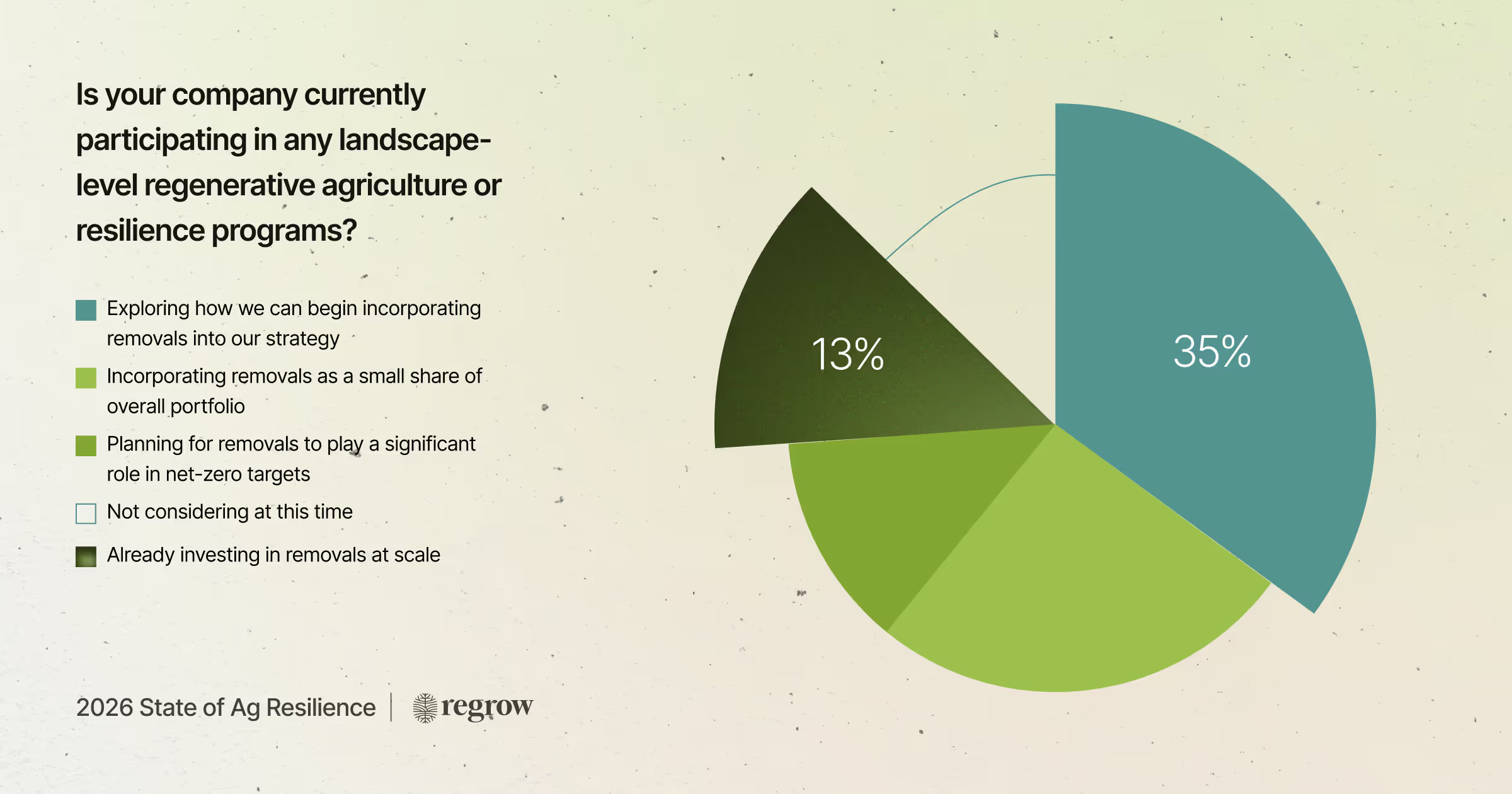

Carbon removals are moving mainstream

Carbon removals are transitioning from exploration toward early adoption. Nearly half of respondents are exploring removals, and more than one-third are already incorporating them into their strategies. Importantly, removals are consistently viewed as a complement to emissions reductions, not a replacement.

Credibility, monitoring, traceability, and permanence remain central concerns. As a result, companies are taking a measured approach: testing methodologies, piloting programs, and building the governance and data foundations needed to support responsible scaling. For some organizations, removals also help stabilize the internal business case for climate investment in years when emissions outcomes fluctuate due to yield variability or external conditions.

Emerging guidance, including LSRS, reinforces the need for clear linkage between field-level practices, quantified outcomes, and supply-chain pathways. Companies that begin building this process discipline now will be better positioned to integrate removals credibly as expectations evolve.

Moving from insight to action

The 2026 State of Agriculture Resilience shows an industry that is increasingly clear-eyed about what resilience requires, and where execution still falls short. Climate risk is being treated as a material business consideration. Data systems are evolving beyond disclosure. Collaboration is gaining momentum, even as partnership design remains complex. Carbon removals are advancing thoughtfully, shaped by a focus on credibility and durability.

What separates leaders from the rest is follow-through. Progress depends on connecting risk assessment to investment, building data systems that can adapt, and designing partnerships that align incentives across sustainability, procurement, and finance.

Resilience is built through deliberate choices: where to focus, which partners to engage, what data truly informs decisions, and how value is defined across the organization. The companies that make these choices with clarity and coordination in 2026 will help define the next phase of agriculture resilience.