.avif)

Contributors

Subscribe to our newsletter

The turning of the calendar to 2024 means we’re officially in the CSRD era.

Data from this fiscal year will be used in the mandatory reporting for 2025, meaning thousands of companies are already on the clock to meet the requirements outlined by the EU’s Corporate Sustainability Reporting Directive (CSRD).

The CSRD is an expansive piece of legislation, coming in at nearly 40,000 words, and requiring reporting across various aspects of environmental, social and governance performance. Those regulated by the CSRD—more than 50,000 organizations—have plenty of work to do in order to achieve compliance next year and beyond.

The CSRD applies to EU-based public and private organizations considered to be “large”— meaning they have two or more of (1) €50 million in net turnover (2) €25 million in assets (3) 250 or more employees.

In this piece, we discuss how CSRD will impact food and agriculture companies, what sustainability leaders can do to ensure success, and how Regrow can help your company achieve compliance.

What is the CSRD?

The Corporate Sustainability Reporting Directive (CSRD) is a landmark piece of legislation enacted by the European Union to promote transparency and accountability in the corporate world.

Through the CSRD, the EU seeks to hold companies accountable for their ESG performance by requiring them to publish data on things like emissions, energy use, diversity, labor rights, and governance structures annually. This data will inform stakeholders about a company’s commitment to sustainability, its progress toward achieving its goals, and opportunities for continued progress.

The CSRD also addresses an area of particular interest to investors: risk exposure. As extreme weather events become more common, organizations will face novel risks that threaten business operations. CSRD reporting data will establish a more transparent and consistent way for the public to determine whether an organization is taking these risks seriously, and building a resilient business.

By providing insight into a company’s ESG practices, the CSRD helps investors, consumers, and other stakeholders make informed decisions about where they put their money. Evidence suggests that companies with higher ESG scores experience lower borrowing rates and enjoy higher public perception around their brand1,2.

When does my company need to complete CSRD reporting?

Large (500+ employee) companies headquartered in the EU will need to report on this year’s data in 2025. Even if you don’t fit the bill for the first wave of disclosures, CSRD is coming if your organization meets the thresholds below.

- Must report on 2025 data: Companies with more than 250 employees and/or 40 million EUR in turnover and/or 20 million EUR in total assets

- Must report on 2026 data: Companies with more than 10 employees and/or more than 700,000 EUR in turnover and/or more than 350,000 EUR in total assets

- For 2028, the CSRD will go international. Non-EU-country companies with a net turnover exceeding 150 million EUR in the EU and a subsidiary or branch in the EU will be included.

How is the CSRD organized?

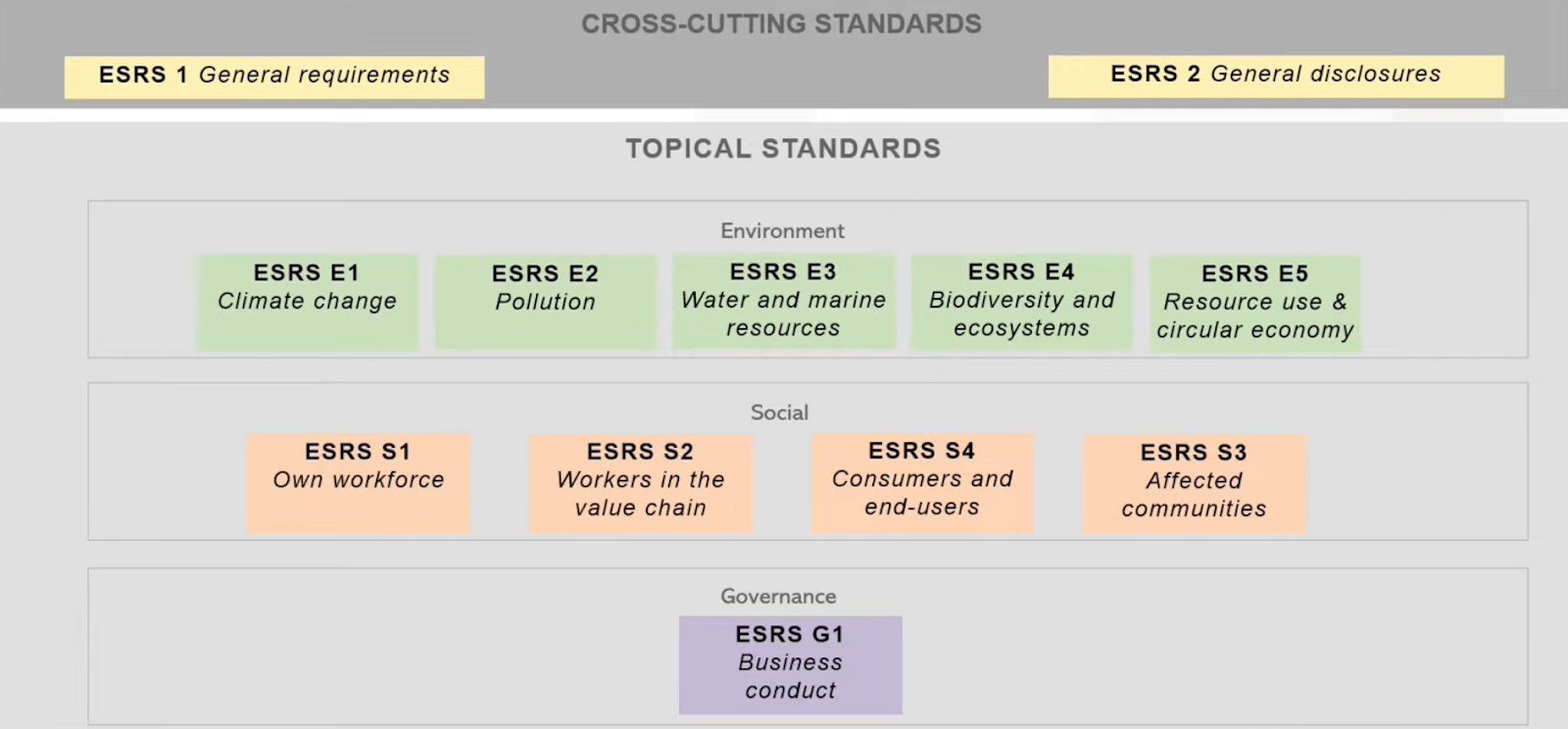

The CSRD establishes 2 ‘cross-cutting’ reporting frameworks, and 10 new topical reporting standards across various environmental, social and governance topics (technically referred to as European Sustainability Reporting Standards).

There are four pillars of reporting that are established in the ‘cross-cutting’ frameworks that inform each topical standard:

- Governance: organizational structures and processes companies use to oversee their sustainability efforts.

- Strategy: the integration of sustainability into both short and long term corporate planning, and the identification of sustainability trends that can affect the business

- Impact, risk, and opportunity management: assessing the company's positive and negative impacts on society and the environment, while also navigating risks and seizing opportunities.

- Metrics and Targets: quantifying sustainability performance and setting ambitious, yet attainable, sustainability goals.

Data Quality and Assurance Requirements

Across the four pillars, the CSRD mandates detailed reporting while maintaining a pragmatic stance on data quality. Sector average data and other proxies are generally permissible, allowing companies some leeway in reporting, particularly in areas where data collection is challenging.

However, in certain domains, such as soil carbon removals, CSRD imposes increased requirements to ensure that reported data genuinely reflects companies' environmental impact.

Specific areas, such as soil carbon removals, are subject to stricter reporting standards to ensure the data's integrity and that companies are not overstating their true environmental impact.

The directive also requires some geographic specificity. For example, companies are asked to provide data breakdowns by country if variations across borders significantly influence risk and opportunity profiles of operations within that region. Companies are also required to disclose any ‘significant sites’ that present material risks (to supply chain integrity, deforestation, working conditions, etc.) , and provide disaggregated reporting data on those specific sites.

This required granularity will be especially pertinent to the food and agriculture sector given how different supply regions and crops can have vastly different responses to a changing climate. Enhancing the precision required in sustainability reports will allow stakeholders to more accurately gauge a company's impact and performance, while also providing internal teams with better insights to prioritize investments that will allow them to meet emissions and other sustainability targets.

Additionally, the CSRD requires companies to receive third party assurance that their reporting is accurate. This mandate begins with a ‘limited assurance’ requirement in 2026, and moves to ‘reasonable assurance’ in 2028.

What topical standards stand out for food & ag companies?

Reporting is required across all ESRS topical standards, but a few are worth diving into further with regards to their impact on food & ag value chain players.

ESRS E1: Climate Change

ESRS E1 covers climate change adaptation, mitigation, and energy use.

One major requirement that will challenge many food & ag companies is the creation of a full inventory of emissions, including a full scope 3 (or value chain) emissions inventory aligned with the Greenhouse Gas Protocol’s accounting standard.

Scope 3 emissions often account for over 90% of total emissions for a packaged food company, with the majority of those emissions occurring in farm driven processes. Those processes have historically been hard to measure at scale. Manual data collection from farmers across a supply shed is costly, time intensive and frequently frustrates both growers and brands. Plus, capturing detailed regional differences in farming practices, soil type and weather poses scientific challenges to the broad brush LCA methods employed by many brands to estimate emissions and other ecological metrics.

ESRS E1 will also reference the forthcoming ‘Carbon Removals Certification Framework’ (CRCF) to determine the aforementioned heightened data requirements for reporting soil carbon removals. CRCF is currently staging a multi stakeholder working group (of which Regrow is a member) to determine the best practices and safeguards for calculating these removals in a robust and conservative manner. A final framework is expected to be released sometime in 2024.

Within the next year, CSRD expects to release a separate agricultural-specific reporting standard which will dictate how companies in the food and ag sectors should account for, and report on, their emissions. We expect this additional standard will incorporate many elements from the Greenhouse Gas Protocol’s forthcoming Land Sector and Removals Guidance (see a draft here).

ESRS E3: Water and Marine Resources + ESRS 4: Biodiversity

The CSRD also establishes new reporting and goal setting requirements for biodiversity and water outcomes. These additional reporting standards reflect an increasing scientific understanding that reducing emissions is not enough. Achieving climate resilience necessitates a holistic approach featuring intentional corporate action to sustain our natural resources.

Like ESRS 1, both ESRS 3 and 4 require companies to evaluate their supply chains, identify and disclose at-risk areas, and establish time-bound plans to achieve relevant milestones. Similarly, higher data granularity is required for geographies that present heightened risk around biodiversity loss, and water quantity or water quality declines.

For water (ESRS 3), beyond the general reporting processes outlined above, the CSRD requires companies to disclose total withdrawal, consumption, and discharge within specified geographic regions and business segments, and set water targets for each of these regions.

For biodiversity (ESRS 4), the CSRD guidance is less prescriptive as biodiversity reporting is comparatively less mature in broadly accepted metrics and data collection methodologies.

However, there is one prescriptive element of the biodiversity reporting requirements: Companies must develop a transition plan detailing a pathway for them to achieve the following milestones:

- No net loss of biodiversity by 2030

- Net biodiversity gain from 2030

- Full recovery of biodiversity by 2050

In coming years, as more reporting requirements and data indicators achieve wider scientific acceptance and become solidified—through governance bodies like the Taskforce for Nature Related Financial Disclosures (TNFD) and Science Based Targets for Nature (SBTN)—we expect the CSRD will adopt certain agreed upon reporting principles.

What steps should I take next?

Here’s a few recommendations, depending on where you are in your CSRD journey…

- “I’d like to see how Regrow can help us achieve CSRD compliance and take action in our supply chains.” We’ve got a team of specialists ready to help. Request a demo here and mention CSRD.

- “I’m not ready to talk, but I am curious to hear more about CSRD reporting specifically.” We’re looking to run a webinar soon going into more detail on how the Regrow platform addresses key concerns of the CSRD. Sign up for our newsletter below to receive an invite to that event once registration is live.

- “I’m good for now, but I’m interested in more insights on food and ag sustainability” Follow Regrow on LinkedIn for regular updates from our team of climate, agronomy and policy experts.