Contributors

Subscribe to our newsletter

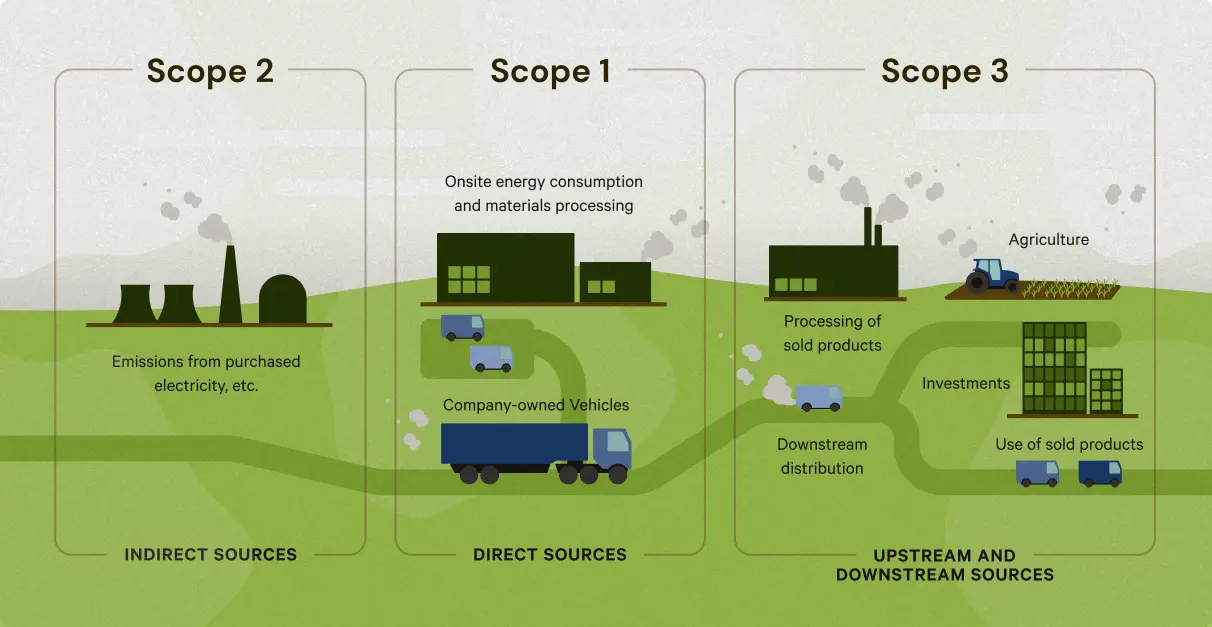

You must address Scope 3 emissions to meet net zero.

According to a recent report by Rabobank, “scope 3 emissions (emissions from the supply chain) account for more than 90% of total emissions for an average packaged food company.” If companies don’t address these emissions, they are unlikely to meet their climate commitments.

Not to mention, we’ll have a hard time meeting our global climate targets and assuring future food supply.

Given this information, one might think it’s simple to prioritize scope 3 emissions. However, scope 3 emissions are difficult to track and measure. How can we reduce our climate impact across nuanced supply chains in a land-based, highly complex industry?

Baseline. Invest. Track. Evolve.

Addressing scope 3 emissions can generally be addressed in four steps:

- Baseline current emissions

- Invest in emission reduction strategies in collaboration with supply chain partners

- Track progress towards climate goals

- Evolve programs to ensure continued success

Although agriculture-based supply chains are nuanced and highly variable, the industry has grown to better support scope 3 emissions reduction, so businesses can move through these steps with more ease and efficiency.

Over the last several years, we’ve seen the industry embrace scope 3 emissions reduction with clearer guidance and more opportunities for collaboration.

Guidance for scope 3 insets has evolved, making investment and action easier.

Until recently, guidance around trading carbon credits (carbon offsetting) was clearer than guidance on climate action within businesses’ own value chains (scope 3 carbon insetting). This lack of clarity has restricted climate-committed corporations — companies are spending too much time searching for clarity, and not enough time building emissions reduction programs.

However, new guidance has emerged to facilitate action. Consider the GHG Protocol Land Sector and Removals Guidance, CDP, and SBTi’s FLAG (Forest, Land and Agriculture) Guidance. These guidelines have set a clearer direction for the industry. While this guidance is still being developed and tested for agriculture, it establishes a runway for pilot projects, partnerships and funding.

It also allows us to engage our scope 3 partners — the businesses and suppliers across supply chains that are ultimately responsible for reducing emissions.

Collaboration brings action.

Reducing scope 3 emissions requires companies to engage partnerships and build win-win business models with suppliers and customers. Scope 3 emissions require cost-sharing with supply chain partners, which can be subject to each partner’s key stakeholders and decision makers.

Through strong partnerships, co-investment and collaboration, we can achieve catalytic climate action. Take, for example, Regrow’s recent work with General Mills and Quantis. Our work together not only allows General Mills to baseline emissions, but it also illuminates a path for other companies to do the same.

This type of collaboration has become more common in the agricultural sector, as companies discover new tools and take advantage of partnerships. If this trend continues, we’ll find that addressing scope 3 emissions is more efficient than expected.

Challenges in guidance and collaboration: risk and co-investment.

However, while guidance and collaboration are clearly supporting the growth of the industry, we recognize that there’s still work to be done. We’ll need to address two key challenges in both these sectors in order to progress our efforts.

Risk can be countered by non-regrettable bets.

It’s difficult for leaders to understand where and how to invest in decarbonization. However, we can simplify our choices and minimize risk with materiality assessments.

Review your company’s materiality assessment to identify the commodities and supply sheds which contribute the highest amount of GHG emissions to your inventory.

Invest in decarbonization programs in those areas, establish an optimal way to motivate your suppliers and gain traction on regenerative agriculture or other sustainable initiatives within your organization.

Co-investment requires sharing climate benefits.

When partners co-invest in resilient farming strategies, they must share the climate benefits. We don’t have guidance for this type of benefit accounting yet… but we are supporting the industry effort to establish such guidance through the Value Chain Initiative! Our science and technology allows us to identify crops and practices on a field and estimate the outcomes of climate-smart farming practices on those fields. Increased development in these areas will help us allocate climate benefits to co-investors.

The industry is exploring a range of solutions.

Several well-qualified industry groups are developing frameworks for co-investment. In the meantime, a few key players are recruiting suppliers and customers to share the costs of emissions reduction, leveraging current guidance and understanding how it might evolve in the near future.

There has also been proposed a contribution-based framework in which companies would make investments into their supply sheds without needing to prove the environmental benefits of the products in their facilities. This would allow the commodity supply chains to remain resilient and flexible, while facilitating investments in emissions reduction.

We share responsibility for change.

Take these challenges as food for thought, and an invitation to collaborate, not a reason to stall climate-smart programs. Establishing a process for reducing scope 3 emissions is difficult, but definitely not impossible.

In the meantime: keep investing, and keep promoting change. Investing in resilience on the farm leads to both ecosystem and community benefits, no matter how you look at it and no matter how you would like to account for it.